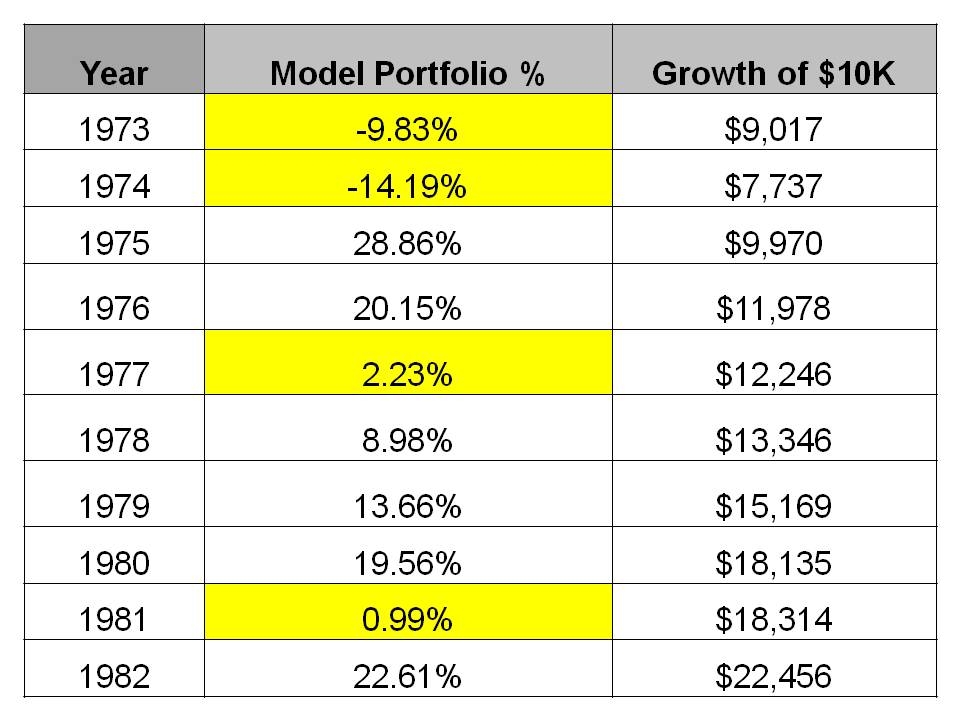

Let’s first consider a $10,000 investment into a diversified portfolio* at the beginning of 1973. In this example a diversified portfolio consists of 60% stocks, 25% bonds, and 15% cash. The chart below documents the annual rate of return of our model portfolio and the growth of our $10,000 investment.

{kind=link}

Despite the significant market pullback of 1973-1974, our $10,000 investment grew to $22,456. This equates to an annualized rate of return of 8.43% over the 10-year period, which many people might find satisfactory. However, let’s examine the growth of our investment after accounting for inflation:

After a decade of nearly double-digit inflation, in real terms our $10,000 investment in 1973 was only worth $9,732 in 1982. Consequently, the annualized real (inflation-adjusted) rate of return achieved by our portfolio over the 10-year period was -0.27%.

After a decade of nearly double-digit inflation, in real terms our $10,000 investment in 1973 was only worth $9,732 in 1982. Consequently, the annualized real (inflation-adjusted) rate of return achieved by our portfolio over the 10-year period was -0.27%. Now let’s explore some potential alternative strategies. First, let’s examine a portfolio consisting of 100% stocks in an attempt to stay ahead of inflation:

{kind=link}

As you can see, when compared to a diversified portfolio a 100% stock allocation was only able to improve the performance of our $10,000 investment by $161 inflation-adjusted dollars over the 10-year period – hardly a significant benefit. At the same time, the 100% stock portfolio was subject to vastly increased volatility. For instance, while the 60% stock, 25% bond, and 15% cash portfolio lost -15.10% and -22.69% in real terms during 1973 and 1974, the 100% stock portfolio lost -22.91% and 33.26% during the same time period. Clearly, the small improvement in return didn’t justify the vastly increased risk.

What if we had attempted a strategy of investing the $10,000 in 3-month Treasury Bills in hopes of keeping up with inflation while avoiding any serious market pullbacks?

Unfortunately, this strategy was unable to spare us the loss experienced by the diversified portfolio. In fact, in real terms the 100% cash approach suffered a loss during seven of the ten years analyzed. Further, history suggests this strategy could never be an effective approach to retirement planning. While a 60% stock, 25% bond, 15% cash portfolio achieved a 5.38% annualized real rate of return from 1970-2010, a portfolio consisting entirely of 3-month Treasury Bills has produced only a 1.08% real return during the same period. Obviously, a 1.08% return is not sufficient to enable most individuals to achieve their investment goals.

Conclusion

In summary, as opposed to making drastic adjustments to a portfolio during the worst 10-year period of inflation in US history, an investor would have been rewarded for sticking with a diversified, buy-and-hold investment approach. No additional advantage would have been gained by making rash changes to the investment strategy. Meanwhile, a diversified model portfolio kept up with inflation as well as any alternative strategy and was well positioned for a market recovery and long term success.

* Model portfolio returns were derived using the following allocation and indexes; STOCKS: 25% DJ Wilshire Large Company Growth Index, 25% DJ Wilshire Large Company Value Index, 10% DJ Wilshire Midcap Growth Index, 10% DJ Wilshire Midcap Value Index, 5% DJ Wilshire Small Company Growth Index, 5% DJ Wilshire Small Company Value Index, 20% Morgan Stanley EAFE Index NR USD; BONDS: 40% Lehman Bros. Long-Credit, 40% Lehman Bros. Long-Term Govt. Bond Index, 20% Citigroup Non-$ World Gov. Bond Index; CASH: 100% 3-Month Treasury Bill

1 comment:

It is very interesting to see the affects of inflation on the different portfolios.

Post a Comment